China's 15th Five-Year Plan: The Green Targets, a New Disclosure Regime, and What They Mean for Global Business

In March 2026, China's National People's Congress approved the 15th Five-Year Plan (FYP), the country's main policy document determining development for the period from 2026 to 2030. For ESG professionals, sustainability investors, and companies with Chinese supply chains, this is one of the most consequential policy documents of the year. The plan is highly supportive of clean energy across the board, but still refrains from setting strong, measurable targets to reduce emissions or fossil fuel consumption. That tension, between massive green investment on one hand and ambiguous emissions commitments on the other, defines the challenge for anyone trying to read China's sustainability trajectory. In this issue, Jaime Amoedo, Executive Director of The ESG Institute, breaks down the key elements of the plan, where the ambition is real, where the gaps remain, and what it means for ESG practice globally.

From Energy Control to Carbon Control

The most significant policy shift in the 15th FYP is structural. China is moving from controlling energy consumption and intensity to controlling carbon emission intensity and total carbon volume. And this is relevant: energy controls measure how much fuel gets burned, carbon controls measure what reaches the atmosphere.

The climate-related objectives are to achieve the goal of carbon peaking as scheduled, to reduce CO2 emissions per unit of GDP by 17% by 2030, and to build a clean, low-carbon, safe and efficient new energy system.

But the 17% intensity target deserves scrutiny. It is lower than the 18% set for the previous five-year period, which itself was missed by a large margin. China's reported annual carbon intensity improvements in 2021 to 2025 only added up to a reduction of 12.4%, putting the country off track from its Paris commitments.

Rather than ramping up efforts, China's decision-makers chose to meet the target by revising past data. The newly suggested definition of CO2 intensity now includes not only energy emissions but also industrial emissions, making it much easier to claim higher emission reductions.

For sustainability analysts and investors, this methodological shift demands attention. Headline numbers may look consistent but the underlying measurement has changed.

The Clean Energy Buildout: Scale Without Precedent

Despite the target debate, the investment scale is staggering.

State Grid, which serves 80% of China, announced plans for 4 trillion yuan (approximately $550 billion) in grid investment over the 15th FYP period, up 40% compared to the 14th Five-Year Plan. Offshore wind power should reach 100 GW by 2030, while nuclear power should rise to 110 GW. Green hydrogen is one of the 10 core new industry levers, with specific plans to accelerate hydrogen production from renewable energy, advance scaled storage and transportation, and push the hydrogen value chain toward green ammonia, methanol, and sustainable aviation fuel.

The plan aims to establish approximately 100 zero-carbon parks and create 10,000 kilometres of zero-carbon transportation corridors. It also targets zero-carbon factories, low-carbon equipment, and industrial clusters that combine renewables, storage, power management, and carbon accounting in one place. Additional targets include achieving energy savings of more than 150 million tonnes of standard coal in key industries and building demonstration projects to replace 30 million tonnes per year of coal consumption in food, textile, and paper-making industries.

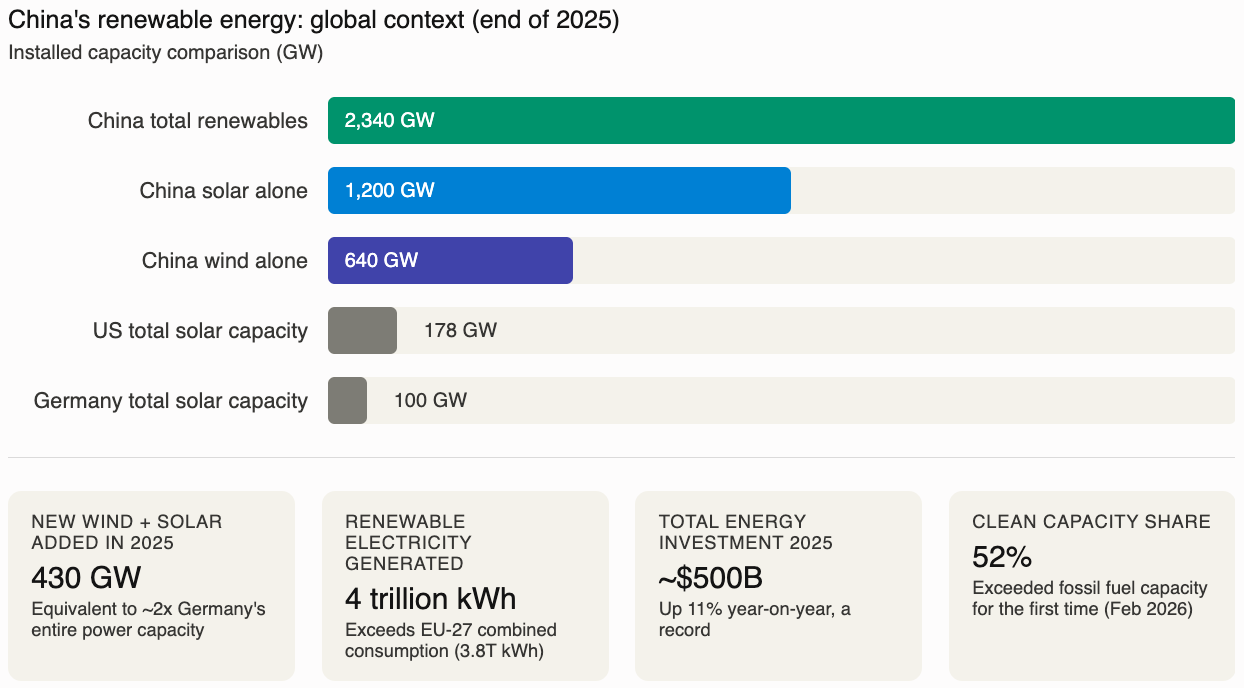

The numbers from 2025 show that this buildout is already underway at extraordinary pace. China added more than 430 GW of new wind and solar capacity in 2025 alone, lifting total installed renewable capacity above 1,800 GW. To put that in perspective, the 430 GW China added in a single year is roughly twice Germany's entire installed power generation capacity. Electricity generation from renewable sources reached about 4 trillion kilowatt-hours in 2025, exceeding the combined power consumption of the EU's 27 member states, which stood at approximately 3.8 trillion kWh.

By the end of 2025, China's solar power capacity had reached 1,200 GW and wind power had reached 640 GW. China's solar additions in the first half of 2025 alone exceeded the entire installed solar base of the United States (178 GW). As of February 2026, China's clean electricity capacity reached 52%, exceeding its fossil fuel-based electricity generation for the first time.

Total energy investment in 2025 topped $500 billion, up 11% year-on-year, a record. In 2024, global investment in renewable energy totalled $2,033 billion. China contributed $625 billion, or 31% of that figure.

For the 15th FYP period, annual new renewable capacity additions are expected to reach 200 to 300 GW per year, sustaining the pace set in 2025.

The Coal Question

The optimism around clean energy collides with a harder reality.

The plan calls for "promoting the peaking" of coal and oil consumption. This is walking back the commitment to gradually reduce coal consumption made by President Xi in 2021, targeting a plateau instead. A statement on "strengthening the clean and efficient utilisation of fossil energy" is included, which is code for the development of the coal-to-chemicals industry, a major driver of China's emissions growth. The plan does not set out a timeline for coal or oil peaking and continues to call for the "clean and efficient" use of coal.

The 2025 data underscores the contradiction. Coal and gas power capacity rose by around 93 GW during the year, 75% more than China added in 2024. Record clean energy additions are running alongside accelerating fossil fuel capacity.

For ESG frameworks that require clear fossil fuel phase-down commitments, this creates a material gap. China is investing more in clean energy than any country on earth while simultaneously keeping the door open for coal expansion in power and chemicals.

ESG Disclosure: A Different Model

The 15th FYP is reshaping ESG disclosure in China, but through a mechanism that looks very different from Western practice.

Rather than asking corporations to self-report against third-party standards, Beijing is mandating ESG integration top-down through industrial policy, performance metrics, and state capital allocation.

Information disclosure should be improved through "legally mandated and voluntary disclosure of enterprise climate information and environmental information." Disclosure may go beyond climate-related reporting and include nature-related disclosure as well.

China's major stock exchanges in Shanghai and Shenzhen jointly issued guidelines for corporate sustainability disclosure, mandating ESG information including Scope 3 emissions and scenario analysis by April 2026. The updates came two years ahead of schedule, indicating that the government attaches great importance to sustainability reporting. This makes China one of the first major economies to require Scope 3 reporting at stock exchange level.

By 2030, China is expected to have a fully embedded national climate disclosure framework. Chinese suppliers will increasingly be required to provide investor-grade climate data. That data will feed directly into requirements such as Streamlined Energy and Carbon Reporting in the UK, the EU's CSRD, and future CBAM-related disclosures.

For companies with Chinese supply chains, the implications are direct.

Green Finance: Continued Acceleration

Green finance will see continued support in the 15th FYP period. The government aims to "enrich green financial products and services, advance carbon finance product and derivative tool innovation, improve the green finance evaluation system for financial institutions, and encourage the increase of investment ratio in green and low-carbon sectors."

The plan introduces a National Low-Carbon Transition Fund, structured with central fiscal guidance and social capital as the main body, operating under a government-led, market-operated model.

China's green loans and green bonds both grew at an average rate of over 20% in the past seven years. This advancement contrasts with trends in many Western markets, which have slowed or, in the case of the United States, reversed progress on green and sustainable finance.

The National ETS: Expanding Scope

China's national Emissions Trading Scheme, already the world's largest by volume of emissions covered, is expanding. Metals and cement were included in the ETS during 2024 and 2025.

China is responsible for 51% of global steel production, 61% of pig iron, and 60% of aluminium. Bringing these sectors into the ETS creates carbon price exposure for a significant share of global industrial output.

The plan calls for non-CO2 greenhouse gas control projects covering methane, nitrous oxide, and hydrofluorocarbons in coal mining, agriculture, waste, and chemical sectors, targeting a reduction of 30 million tonnes of CO2 equivalent.

What This Means for Global ESG Practice

The 15th FYP matters beyond China's borders. Several practical implications stand out for ESG professionals worldwide.

Supply chain disclosure is accelerating. Companies sourcing from China will face increasing pressure to integrate Chinese supplier ESG data into their own reporting frameworks, particularly under CSRD and CBAM.

Carbon market exposure is growing. The expansion of China's ETS into steel, cement, and metals creates carbon price signals across global supply chains. Companies with Scope 3 exposure to Chinese manufacturing need to factor this into risk assessments.

Green finance is diverging. While some Western markets are retreating from ESG commitments, China is accelerating. The creation of a National Low-Carbon Transition Fund and continued expansion of green bond and green loan markets signal a market that global sustainable finance teams cannot ignore.

Intensity targets vs. absolute targets. The absence of absolute emission reduction targets remains a challenge for institutional investors whose ESG frameworks require hard caps. Portfolio managers need to assess whether China's intensity-based approach is compatible with their fund mandates and Paris-alignment claims.

The definition of ESG is different. Beijing is mandating ESG integration top-down through industrial policy and state capital allocation, not through the voluntary disclosure frameworks familiar in Europe and North America. ESG teams need to understand that the same objectives are being pursued through fundamentally different mechanisms.

The Bottom Line

China's 15th Five-Year Plan is one of the most ambitious green investment programmes any country has ever put on paper. $550 billion in grid investment alone. 100 GW offshore wind by 2030. Scope 3 disclosure mandated at stock exchange level two years ahead of schedule. The clean energy buildout is real, it is funded, and it is already delivering results at a scale no other economy can match.

The plan also leaves important questions open. The 17% carbon intensity target is softer than its predecessor. Coal retains a role in the energy mix without a defined exit timeline. The methodology behind the baseline has shifted.

For sustainability professionals, the opportunity is to engage with both sides of that picture. The green investment creates commercial pathways in clean energy, carbon markets, and sustainable finance. The open questions around absolute emissions and fossil fuel commitments mean due diligence and careful analysis remain essential.

China is definitely moving. The direction is clear. The pace and completeness of the transition are what the next five years will determine.

Stay Ahead of the ESG Curve

At The ESG Institute, we empower professionals and organisations to navigate the world's evolving sustainability regulations with clarity and confidence. From ESG reporting frameworks and governance, to carbon markets, sustainable finance, and enterprise risk management, our accredited online programmes and advisory services are designed to turn compliance into opportunity.

Our programmes span ESG strategy, sustainability reporting, carbon markets, climate law, sustainable finance, CSRD compliance, and more, equipping professionals with the practical tools to translate materiality into the kind of decision-ready outputs that boards, investors, and finance teams can act on.

Explore our globally recognised diplomas and certificates, all fully online and CPD-accredited.

Learn more at www.the-esg-institute.org/training and join a growing community of over 10,000 sustainability alumni shaping a better future.

For personalized guidance on integrating sustainability into your business operations, reach out to The ESG Institute. Our experts are here to help you navigate the complexities of ESG implementation and drive meaningful change.