Europe Redraws the Carbon Market. What the Revised Climate Law Means for Global Business

In this interview, Jaime Amoedo, Executive Director and Co-founder of The ESG Institute, explains the implications of the European Union’s latest amendment to the European Climate Law, which introduces a legally binding 90 percent emissions reduction target by 2040 and, for the first time, allows the use of international carbon credits under Article 6 of the Paris Agreement.

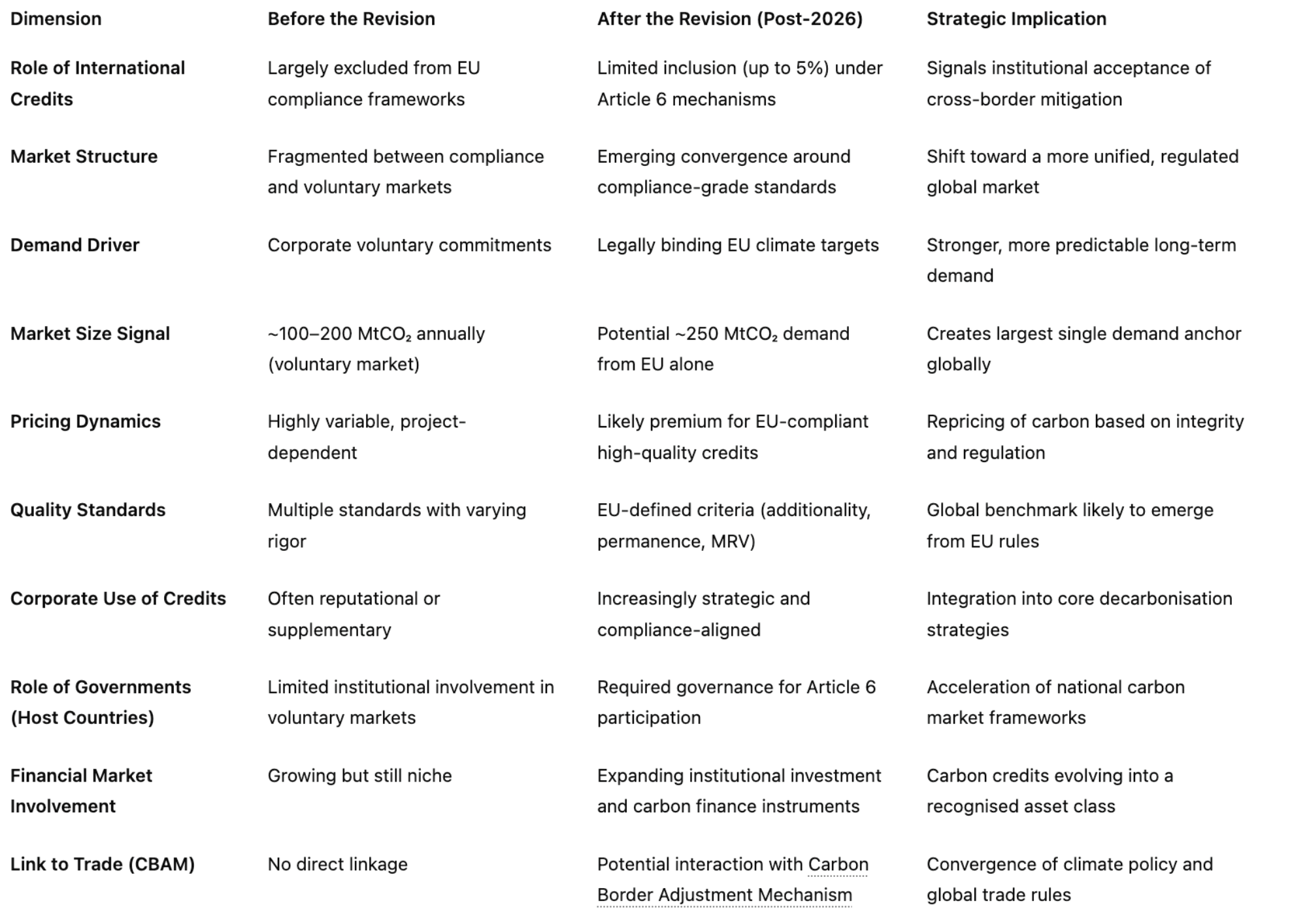

This marks a significant shift in the EU’s climate strategy. While the Union has historically excluded international credits from its compliance framework, the new law opens the door to their limited use, up to 5 percent of the 2040 target. In practical terms, this could translate into demand for approximately 250 million tonnes of CO₂ equivalent.

In this edition of The Sustainability Gazette, we explore what this change means for carbon markets, corporates, and governments worldwide, and why it may redefine how global climate finance operates.

Jaime, the EU has introduced a 90 percent emissions reduction target for 2040, but much of the discussion is focused on the inclusion of Article 6 credits. Why is this element so significant?

The headline target is ambitious, but not entirely unexpected. The European Union has consistently positioned itself as a leader in climate policy. What is new, and genuinely transformative, is the decision to allow international carbon credits into its compliance architecture.

For years, the EU maintained a strict position. Emissions reductions had to be achieved domestically, supported by mechanisms such as the EU Emissions Trading System. International credits were viewed with caution due to concerns around credibility and accounting integrity.

What we are seeing now is a recalibration. The EU is acknowledging that achieving deep decarbonisation, particularly in sectors where emissions are difficult to eliminate, may require some degree of international cooperation. But importantly, this is not a relaxation of standards. It is a controlled opening, where the EU intends to define what high-quality credits look like.

The figure of 250 million tonnes of CO₂ equivalent has been widely cited. How should we interpret this from a market perspective?

It is a very large number in the context of carbon markets.

To put it into perspective, the voluntary carbon market has historically operated at a scale that is comparable or even smaller than that figure on an annual basis. What the EU is effectively doing is introducing a compliance-driven demand signal that could exceed the size of the existing voluntary market.

That changes the dynamics entirely. Markets respond to predictable demand, especially when it is anchored in regulation. This creates a strong incentive for project developers, investors, and governments to position themselves for future supply.

It also introduces a new benchmark. Credits that meet EU standards will likely be treated very differently from those that do not. We could see a clear separation between high-integrity credits and the rest of the market.

Does this mean we are moving from voluntary carbon markets to something closer to a regulated global system?

We are certainly moving in that direction.

Until now, voluntary markets have played an important role, particularly in enabling corporate climate action. However, they have also faced persistent challenges around transparency, standardisation, and trust.

By introducing regulated demand, the EU is effectively anchoring part of the carbon market in law. That brings with it higher expectations around quality, governance, and verification.

It does not mean voluntary markets will disappear. But it does mean that their role will evolve. The centre of gravity is shifting towards compliance-grade markets, where credibility is not optional, it is enforced.

Can you explain how Article 6 works in practice, particularly for readers who may not be familiar with it?

At its core, Article 6 provides a framework for countries to cooperate in reducing emissions.

Take a simple example. Imagine a renewable energy project in a developing country that replaces fossil fuel-based electricity generation. That project generates measurable emissions reductions. Under Article 6.2, those reductions can be transferred to another country, provided that the host country adjusts its own emissions accounting accordingly. This is what we call a corresponding adjustment, and it is essential to avoid double counting.

There is also Article 6.4, which establishes a centralised mechanism for issuing credits, somewhat similar to earlier systems but with more robust rules.

In practice, this creates a system where capital can flow to projects that deliver real emissions reductions, while ensuring that the accounting remains transparent and credible.

What are the implications for project developers and host countries?

The most immediate implication is opportunity, but it comes with responsibility.

Project developers now have a clearer signal that there will be demand for high-quality credits in the future. This encourages investment in new projects, whether in renewable energy, industrial decarbonisation, or nature-based solutions.

However, the bar will be higher. Developers will need to demonstrate that their projects meet stringent criteria around additionality, permanence, and verification.

For host countries, the challenge is institutional. Participating in Article 6 requires governance frameworks, approval processes, and systems to track emissions reductions and apply corresponding adjustments. Countries that move early and build this infrastructure will be better positioned to attract investment and participate in these markets.

How does this affect companies, particularly those outside the EU?

This is where the global impact becomes very clear.

Even if a company is not based in the EU, it may still be exposed through supply chains, investors, or market access. European stakeholders are increasingly demanding credible climate strategies, and this will now include how companies engage with carbon markets.

For many organisations, carbon credits have been treated as a secondary tool, often used at the end of a reporting cycle. That approach is becoming outdated. Companies will need to think more strategically about how they integrate carbon markets into their overall decarbonisation plans.

We are already seeing this in practice. Multinational companies are exploring how high-quality credits can support their Scope 3 strategies, particularly where direct reductions are difficult to achieve.

There has also been discussion about the interaction with CBAM. How do you see that evolving?

The Carbon Border Adjustment Mechanism is already reshaping trade by introducing a carbon cost on certain imports. The potential interaction with Article 6 credits adds another layer of complexity.

While the details are still being developed, there is a broader trend towards convergence. Climate policy, trade policy, and carbon markets are becoming more interconnected.

For exporting countries and companies, this means that carbon is no longer just an environmental issue. It is becoming a factor in competitiveness and market access. Aligning with credible carbon accounting systems and, potentially, international credit mechanisms could become a strategic necessity.

A key question remains around quality. What defines a “high-quality” carbon credit in this new context?

That is the central question, and it will largely be answered by the European Commission in the coming years.

We can expect the criteria to focus on well-established principles. Additionality is fundamental. The emissions reduction must not have occurred without the project. Permanence is critical, particularly for nature-based solutions. There must also be strong safeguards against leakage, where emissions are simply shifted elsewhere.

Equally important are monitoring, reporting, and verification systems. The EU will require a level of transparency and auditability that aligns with its broader regulatory framework.

Striking the right balance will be essential. If the standards are too restrictive, supply may be limited. If they are too lenient, credibility will be undermined. The EU’s decisions here will likely influence global standards.

What role do you see financial markets playing in this transition?

A very significant one.

Carbon credits are increasingly being viewed as an asset class. We are seeing the emergence of carbon-focused investment funds, as well as growing interest from institutional investors.

There is also a shift towards more sophisticated financial instruments, such as forward contracts, which allow buyers to secure future supply at known prices. This is particularly relevant in a market where demand is expected to increase and supply may take time to scale.

In many ways, we are witnessing the financialisation of carbon markets, but with a stronger emphasis on environmental integrity.

Looking ahead, what are the key risks and uncertainties?

There are several.

Regulatory uncertainty is one. The details of how Article 6 credits will be integrated into the EU framework are still being developed. Delays or complexity could affect market confidence.

Supply is another concern. High-quality projects take time to develop, and there may be a gap between demand and available credits in the early years.

There are also integrity risks. Carbon markets have faced criticism in the past, and maintaining trust will be essential. Any perception that low-quality credits are being used could undermine the system.

Finally, there are geopolitical factors. Not all countries are at the same stage in developing Article 6 frameworks, and coordination will be key.

What should businesses, governments, and investors be doing now to prepare?

The most important step is to recognise that this is not a distant issue. The timeline may extend to 2031 and beyond, but decisions made today will determine positioning in the future.

Governments should focus on building the institutional frameworks required to participate in Article 6. This includes governance, transparency, and capacity building.

Businesses need to move beyond a compliance mindset and integrate carbon markets into their broader strategies. This means understanding how credits work, where they come from, and how they align with corporate objectives.

Investors should be looking at long-term opportunities, particularly in project development and infrastructure.

Across all of these groups, knowledge and capability will be critical.

What role does The ESG Institute play in supporting this transition?

Our role is to translate complexity into practical understanding.

Carbon markets are evolving rapidly, and many professionals do not yet have the tools or knowledge to navigate them effectively. That is why we developed the Diploma in Carbon Markets & Climate Finance.

The programme is designed to provide a comprehensive understanding of both compliance and voluntary markets, including Article 6 mechanisms, carbon pricing, and financial instruments. It is not just theoretical. It focuses on real-world application, which is what professionals need in this space.

As these markets become more structured and integrated into regulation, having that expertise will be increasingly valuable.

Finally, what is your key message to the market?

The message is that we are entering a new phase.

Carbon markets are becoming part of the core architecture of climate policy and global finance. The European Union’s decision accelerates that transition.

Those who understand how these systems work, and who engage early, will be better positioned. Those who wait may find themselves reacting to changes rather than shaping them.

At The ESG Institute, we believe that informed decision-making is the foundation of effective sustainability strategy. This is a moment where knowledge will define leadership.

Table: How the EU’s Revised Climate Law Reshapes Carbon Markets

For more information: 2040 climate target: Council gives final green light

Ready to take your career to the next level? Explore here our training programs, including the Diploma in Carbon Markets & Climate Finance, and the Diploma in CBAM Regulation, and gain the expertise needed to navigate the evolving landscape of global carbon markets..

For personalized guidance on integrating sustainability into your business operations, reach out to The ESG Institute. Our experts are here to help you navigate the complexities of ESG implementation and drive meaningful change.