From Decree to Emergency Plan: Spain Bets Big on ESG

Spain’s climate policy is entering a decisive new phase. With the adoption of Royal Decree 214/2025 and the launch of the Climate Emergency Plan, the country has shifted from voluntary reporting and incremental measures to a binding framework that combines carbon accountability, Scope 3 integration, and national resilience strategies. While much of Europe is slowing down or diluting ESG requirements, Spain is accelerating, turning climate responsibility into a core compliance and competitiveness issue. At The Sustainability Gazette, we explore how these measures raise the bar for companies and public institutions alike, why Spain’s approach stands out in the current European landscape, and what this means for businesses preparing to navigate stricter obligations. From carbon reporting standards to adaptation mandates and investment opportunities, this article unpacks Spain’s bold step toward embedding ESG compliance at the heart of its economic and environmental strategy.

Europe is at a crossroads in climate and sustainability policy. On one side, the European Union has chosen to simplify and delay parts of its ambitious Corporate Sustainability Reporting Directive (CSRD) through the Omnibus package. The goal, according to Brussels, is to ease the compliance burden and protect competitiveness. On the other side, Spain has taken the opposite approach. With its recent Royal Decree 214/2025 and the subsequent Climate Emergency Plan, the Spanish government is pressing forward with mandatory carbon reporting, Scope 3 integration, resilience measures, and the creation of new institutions to manage the climate crisis.

At a time when political hesitation and pushback against ESG are growing louder across Europe, Spain has shown that ambition can be matched with decisive legislative action. This is not a symbolic gesture; it is the construction of a comprehensive framework that transforms climate responsibility into a binding legal reality for companies and public institutions.

To understand the significance of this moment, it is important to revisit the foundations laid by the Royal Decree in April 2025 and then analyze how the Climate Emergency Plan extends, deepens, and broadens those obligations. Together, they form one of the most robust national ESG frameworks in Europe.

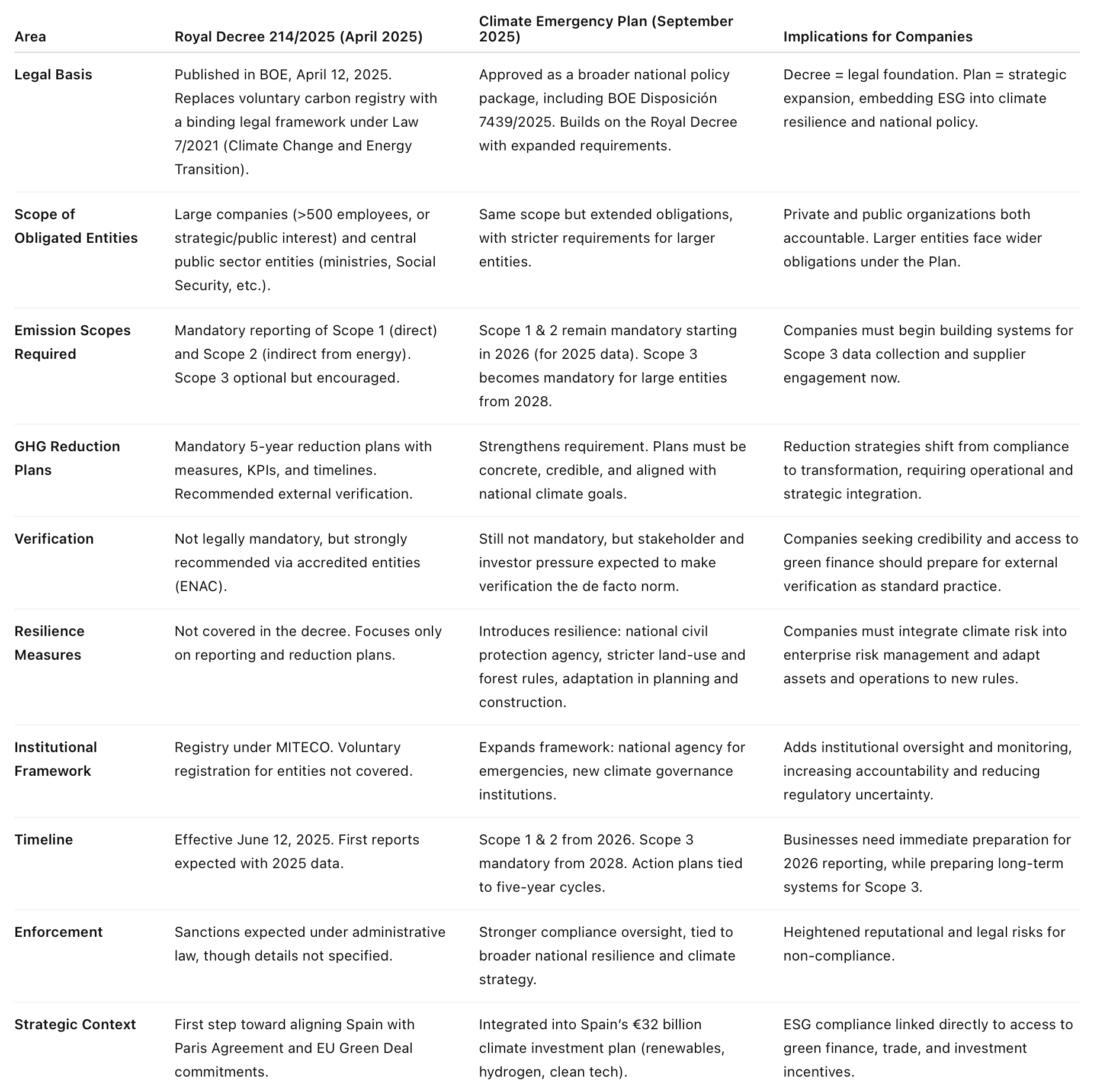

Royal Decree 214/2025: The Legal Foundation

Published in the Official State Gazette (BOE) on April 12, 2025, Royal Decree 214/2025 marked the beginning of a new era for corporate climate accountability in Spain. It repealed earlier voluntary frameworks and introduced mandatory requirements for large companies and public sector entities.

Who Must Comply

The decree applies to two categories:

Large private sector entities: Companies preparing consolidated financial statements under Spanish law, especially those with more than 500 employees, fall under this obligation. In addition, companies deemed strategic or of public interest must comply, even if they do not meet the employee threshold.

Public sector entities: Ministries, government departments, Social Security bodies, and other institutions within the central government must also measure and disclose their carbon footprint.

This dual scope signaled that accountability was not limited to the private sector. The government itself placed public institutions under the same requirements, demonstrating that climate responsibility is a shared obligation.

Technical Requirements

The decree requires organizations to calculate their carbon footprint according to internationally recognized standards. Companies can choose between ISO 14064-1:2018 or the Greenhouse Gas Protocol, both of which ensure consistency, comparability, and transparency.

Reports must define organizational boundaries, clarifying which entities within a group are included, and operational boundaries, specifying whether control is determined by financial ownership, equity share, or operational authority.

The emissions inventory must include:

Scope 1: Direct emissions from sources owned or controlled by the organization.

Scope 2: Indirect emissions from purchased energy.

Scope 3 emissions, which account for the broader value chain, are strongly encouraged but remained voluntary under the decree.

Companies must also establish a base year as a benchmark for tracking emissions reductions over time. This ensures continuity and allows stakeholders to monitor progress against a consistent reference point.

Reduction Plans

A mandatory component of the decree is the requirement to prepare greenhouse gas reduction plans. These plans must set out technical and strategic measures to cut emissions, specify timelines, and identify key performance indicators. Responsibility for execution must be assigned internally.

Although external verification is not required, it is strongly recommended. Independent validation, preferably by accredited organizations such as ENAC, enhances the credibility of reported data and helps prevent accusations of greenwashing.

Implementation Timeline

The decree came into effect on June 12, 2025, just two months after publication. For many organizations, this represented an extremely tight deadline, particularly given the complexity of emissions accounting. Large companies were advised to begin preparation immediately to avoid penalties and reputational risk.

Voluntary Opportunities

The decree also left the door open for organizations not formally required to comply. The national carbon footprint registry, managed by the Ministry for Ecological Transition (MITECO), remains open for voluntary submissions. For smaller companies, this represents a strategic opportunity to demonstrate leadership, enhance reputation, and prepare for future regulatory changes.

Royal Decree 214/2025 was, therefore, both a binding framework and a gateway to broader engagement. It established the minimum expectations while encouraging voluntary action.

The Climate Emergency Plan: Raising the Ceiling

Where the decree created the legal foundation, the Climate Emergency Plan builds the superstructure. It significantly expands obligations, tightens timelines, and incorporates resilience measures that go well beyond emissions reporting.

Scope 1 and 2 Obligations

Companies will need to report Scope 1 and Scope 2 emissions starting in 2026, using data from 2025. This builds directly on the decree but provides more clarity and enforcement.

Mandatory Scope 3 Reporting

Perhaps the most transformative element of the plan is the phased introduction of Scope 3 reporting. From 2028, large companies must include value chain emissions in their disclosures. This is a decisive break with the past, recognizing that for most organizations Scope 3 accounts for the majority of their climate impact.

Making Scope 3 mandatory will force companies to map, monitor, and influence their supply chains. It will require collaboration with suppliers, integration of new technologies for data management, and stronger engagement with stakeholders. For many businesses, this will be the most challenging aspect of the plan, but also the most impactful.

Greenhouse Gas Reduction Plans

The plan makes reduction strategies more than a formality. Companies must submit concrete, five-year action plans that go beyond aspiration. These plans must include detailed measures, measurable outcomes, and accountability structures. They are to be aligned with national climate goals, creating a direct link between corporate action and Spain’s Paris Agreement commitments.

Resilience and Adaptation

The Climate Emergency Plan extends beyond emissions. It recognizes that Spain is already experiencing the consequences of climate change, from extreme heatwaves to droughts and wildfires. To address these risks, the plan introduces:

A new national agency for civil protection and emergencies, tasked with coordinating responses to climate-related disasters.

Stricter land-use and forest management rules, designed to reduce vulnerability to fires and floods.

Requirements for local adaptation strategies, ensuring that regions integrate climate risks into urban planning, construction codes, and infrastructure development.

This holistic approach ensures that mitigation and adaptation are treated as two sides of the same coin.

Energy and Investment

The Climate Emergency Plan is not only about regulation; it is also tied to an ambitious investment strategy. The Spanish government has committed billions of euros to renewable energy, green hydrogen, and clean technology. The aim is to achieve 100 percent renewable electricity by 2050, reduce emissions by 32 percent by 2030, and reach 81 percent renewable energy in power generation.

This integration of regulatory obligations with economic opportunity underscores the strategic nature of the plan. It is not simply a compliance exercise but a vision for Spain’s future economy.

Spain Versus Europe: Diverging Paths

The contrast with Brussels could not be sharper. The EU Omnibus package has delayed parts of the CSRD and reduced the reporting burden for many companies. Its stated aim is to enhance competitiveness and streamline requirements. Critics argue that it weakens Europe’s global leadership in sustainability.

Spain, however, has taken the view that ambition drives competitiveness, not the other way around. By moving faster and deeper, it is betting that companies which adapt to higher standards will be more resilient, more attractive to investors, and better aligned with the global transition to a low-carbon economy.

This divergence reveals the emergence of a multi-speed Europe. The EU sets the floor, but member states can raise the ceiling. Spain is demonstrating that national governments can and should go further when the urgency of climate change demands it.

For companies operating across borders, this creates complexity. They will have to navigate both EU-level directives and stricter national rules. But it also creates an opportunity. By complying with Spain’s higher standards, companies will be ahead of the curve and well prepared for future global convergence.

Implications for Business

The implications for businesses in Spain are profound.

First, Scope 3 preparation must begin immediately. Waiting until 2028 will be too late. Companies need to build supplier engagement programs, invest in digital tools for emissions tracking, and start collecting value chain data now.

Second, greenhouse gas reduction plans must be credible and detailed. Regulators, investors, and the public will not accept vague commitments. Companies should integrate reduction strategies into their overall corporate governance, assign responsibility at board level, and monitor progress with measurable indicators.

Third, resilience must be taken seriously. Businesses should assess their exposure to climate risks, integrate adaptation into enterprise risk management, and align with the new national resilience framework.

Fourth, companies that embrace these requirements proactively will find themselves better positioned to attract sustainable finance, improve ESG ratings, and strengthen stakeholder trust. What may appear at first as a compliance burden is, in fact, an opportunity to lead.

Conclusion

Spain’s decision to double down on ESG compliance is important for three reasons.

It demonstrates political will. At a time when climate ambition is contested, Spain has shown that governments can take decisive action and hold both the private and public sectors accountable.

It integrates mitigation and adaptation. By combining emissions reporting with resilience measures, Spain acknowledges that climate action is not only about reducing carbon but also about preparing for unavoidable impacts.

It links regulation with strategy. By embedding ESG requirements in a broader investment and energy transition agenda, Spain is showing that climate policy is an engine of economic competitiveness, not a drag on it.

Spain’s journey from Royal Decree 214/2025 to the Climate Emergency Plan represents one of the most ambitious national sustainability frameworks in Europe today. Together, these measures require companies to measure, disclose, reduce, and adapt. They bind public institutions to the same standards. They create new agencies and resilience structures. And they connect climate responsibility with investment in clean technology and renewable energy.

At The ESG Institute, we view this as a turning point. Spain is proving that ambition and competitiveness are not mutually exclusive but mutually reinforcing. The EU may set the floor, but Spain has set the ceiling. The rest of Europe would do well to take note.

For readers who want to revisit the foundation of these developments, our April article on Royal Decree 214/2025 can be found here: Spain’s New Royal Decree 214/2025: Mandatory Carbon Footprint Reporting is Here. This follow-up shows how that decree has now evolved into a broader Climate Emergency Plan.

The question now is not whether companies should comply, but how quickly they can adapt and how strategically they can position themselves in a world where ESG leadership is becoming a competitive necessity.

Key Takeaways

From Voluntary to Binding: The Royal Decree ended Spain’s voluntary carbon registry. The Climate Emergency Plan pushes further, turning Scope 3 from a recommendation into a legal obligation.

From Reporting to Resilience: The decree focused on emissions accounting. The plan integrates resilience, civil protection, and land-use governance.

From Compliance to Competitiveness: Spain is positioning ESG obligations not as costs but as a pathway to green investment and competitiveness in the global economy.

Timeline Pressure: Companies face immediate requirements for Scope 1 and 2, with just over two years to prepare for mandatory Scope 3.

Higher Standards, Higher Opportunity: Spain’s framework raises the bar well above the EU’s minimum. Businesses that adapt early will strengthen market positioning, access finance more easily, and build trust with stakeholders.

Annex: Royal Decree 214/2025 vs. Climate Emergency Plan

Spanish Version - De Real Decreto a Plan de Emergencia Climática: España apuesta fuerte por el ESG

Europa se encuentra en una encrucijada en materia de política climática y de sostenibilidad. Por un lado, la Unión Europea ha optado por simplificar y retrasar parte de su ambiciosa Directiva de Informes de Sostenibilidad Corporativa (CSRD) a través del paquete Omnibus. El objetivo, según Bruselas, es aliviar la carga de cumplimiento y proteger la competitividad. Por otro lado, España ha tomado el camino contrario. Con su reciente Real Decreto 214/2025 y el posterior Plan de Emergencia Climática, el gobierno español avanza con firmeza hacia el reporte obligatorio de emisiones de carbono, la integración del Alcance 3, medidas de resiliencia y la creación de nuevas instituciones para gestionar la crisis climática.

En un momento en el que las dudas políticas y la resistencia frente al ESG se hacen cada vez más fuertes en Europa, España ha demostrado que la ambición puede ir acompañada de acción legislativa decisiva. No se trata de un gesto simbólico, sino de la construcción de un marco integral que convierte la responsabilidad climática en una realidad legalmente vinculante para empresas e instituciones públicas.

Para comprender la importancia de este momento, es fundamental revisar las bases sentadas por el Real Decreto de abril de 2025 y analizar cómo el Plan de Emergencia Climática amplía, profundiza y refuerza dichas obligaciones. Juntos, conforman uno de los marcos ESG nacionales más sólidos de Europa.

Real Decreto 214/2025: la base legal

Publicado en el Boletín Oficial del Estado (BOE) el 12 de abril de 2025, el Real Decreto 214/2025 marcó el inicio de una nueva era para la rendición de cuentas climática empresarial en España. Derogó los marcos voluntarios previos e introdujo requisitos obligatorios para las grandes empresas y las entidades del sector público.

¿Quién debe cumplir?

El decreto se aplica a dos categorías:

Grandes empresas privadas: aquellas que elaboran cuentas consolidadas conforme a la legislación española, en particular las que cuentan con más de 500 empleados. Además, también deben cumplir las empresas consideradas estratégicas o de interés público, incluso si no alcanzan dicho umbral.

Entidades del sector público: ministerios, departamentos gubernamentales, entidades de la Seguridad Social y otros organismos dependientes de la Administración central deben medir y divulgar su huella de carbono.

Este doble alcance reflejó que la rendición de cuentas no se limita al sector privado. El propio gobierno se sometió a las mismas exigencias, demostrando que la responsabilidad climática es compartida.

Requisitos técnicos

El decreto exige calcular la huella de carbono de acuerdo con estándares internacionalmente reconocidos. Las empresas pueden optar entre la norma ISO 14064-1:2018 o el Protocolo de Gases de Efecto Invernadero (GHG Protocol), ambos garantes de consistencia y transparencia.

Los informes deben definir los límites organizacionales y operacionales, aclarando qué entidades del grupo están incluidas y qué tipo de control (financiero, operativo o por participación accionarial) se utiliza como referencia.

El inventario de emisiones debe abarcar:

Alcance 1: emisiones directas de fuentes propias o controladas.

Alcance 2: emisiones indirectas procedentes de la energía adquirida.

Alcance 3: emisiones de la cadena de valor, que permanecían voluntarias pero fuertemente recomendadas.

Las empresas deben además establecer un año base como referencia para evaluar la evolución de sus reducciones.

Planes de reducción

Un componente clave del decreto es la obligación de elaborar planes de reducción de gases de efecto invernadero. Dichos planes deben detallar medidas técnicas y estratégicas, fijar cronogramas, definir indicadores y asignar responsabilidades internas.

Aunque la verificación externa no es obligatoria, se recomienda de manera enfática. La validación independiente, preferiblemente a través de organismos acreditados como ENAC, refuerza la credibilidad de los datos y reduce riesgos de greenwashing.

Calendario de implementación

El decreto entró en vigor el 12 de junio de 2025, apenas dos meses después de su publicación. Para muchas organizaciones, representó un plazo ajustado, dada la complejidad del cálculo de emisiones.

Oportunidades voluntarias

El decreto también dejó abierta la posibilidad de participación voluntaria. El registro nacional de huella de carbono, gestionado por el MITECO, sigue disponible para empresas no obligadas. Para las pymes, supone una oportunidad estratégica de demostrar liderazgo y prepararse para futuros cambios regulatorios.

En definitiva, el Real Decreto 214/2025 estableció un marco vinculante mínimo y, al mismo tiempo, un canal para fomentar el compromiso voluntario.

El Plan de Emergencia Climática: elevando el nivel

Si el decreto creó la base legal, el Plan de Emergencia Climática construye el andamiaje superior. Amplía obligaciones, endurece plazos e incorpora medidas de resiliencia que van mucho más allá del reporte de emisiones.

Alcances 1 y 2

Las empresas deberán reportar Alcance 1 y Alcance 2 a partir de 2026, con datos correspondientes a 2025. Esto refuerza lo ya previsto en el decreto y añade claridad sobre la exigibilidad.

Alcance 3 obligatorio

El elemento más transformador es la incorporación progresiva del Alcance 3. Desde 2028, las grandes compañías deberán incluir en sus informes las emisiones de la cadena de valor. Para la mayoría de organizaciones, estas representan el grueso de su impacto climático.

Esto obligará a mapear proveedores, invertir en herramientas digitales de seguimiento y reforzar la colaboración con toda la cadena de suministro. Será probablemente el mayor reto del plan, pero también la medida más trascendental.

Planes de reducción de GEI

El plan convierte los planes de reducción en un requisito sustantivo. Las empresas deben presentar acciones quinquenales concretas, con medidas detalladas, resultados medibles y estructuras claras de responsabilidad. Deben además estar alineadas con los objetivos climáticos nacionales.

Resiliencia y adaptación

El plan reconoce que España ya enfrenta impactos climáticos graves: olas de calor, sequías e incendios forestales. Por ello, incluye:

Creación de una agencia nacional de protección civil y emergencias para coordinar respuestas.

Normas más estrictas en gestión forestal, uso del suelo y edificación en zonas de riesgo.

Estrategias de adaptación locales obligatorias, integradas en la planificación urbana y de infraestructuras.

Energía e inversión

El Plan de Emergencia Climática se acompaña de un programa inversor millonario en energías renovables, hidrógeno verde y tecnologías limpias. Los objetivos son claros: 100% de electricidad renovable en 2050, reducción del 32% de emisiones en 2030 y alcanzar un 81% de renovables en la generación eléctrica.

Se trata, por tanto, de una estrategia regulatoria y económica al mismo tiempo.

España frente a Europa: caminos divergentes

El contraste con Bruselas es evidente. Mientras la UE retrasa requisitos del CSRD para aligerar cargas, España apuesta por profundizar en la regulación. Para el gobierno español, la ambición no resta competitividad, la impulsa.

Esto muestra una Europa a varias velocidades. La UE fija el suelo, pero cada Estado miembro puede elevar el techo. España ha demostrado que no solo se puede ir más allá, sino que es necesario cuando la urgencia climática lo exige.

Conclusión

Las consecuencias para el tejido empresarial español son inmediatas:

La preparación para el Alcance 3 debe comenzar ya. Esperar a 2028 sería demasiado tarde.

Los planes de reducción deben ser verificables, ambiciosos y medibles.

La resiliencia debe integrarse en la gestión de riesgos corporativos.

Las compañías que actúen con anticipación accederán a mejores condiciones de financiación sostenible, mejorarán su posicionamiento ESG y reforzarán la confianza de sus grupos de interés.

La decisión de España de reforzar el cumplimiento ESG tiene tres grandes virtudes: demuestra voluntad política, integra mitigación y adaptación, y vincula regulación con estrategia económica.El recorrido desde el Real Decreto 214/2025 hasta el Plan de Emergencia Climática representa hoy uno de los marcos de sostenibilidad más ambiciosos de Europa. Obliga a medir, divulgar, reducir y adaptarse. Vincula a entidades públicas y privadas. Crea nuevas instituciones y conecta la responsabilidad climática con la transformación económica verde.

En The ESG Institute consideramos que este es un punto de inflexión. España demuestra que la ambición y la competitividad no son excluyentes, sino complementarias. La UE podrá fijar el mínimo, pero España ha marcado el máximo.

Para quienes deseen repasar las bases de este proceso, nuestro artículo de abril sobre el Real Decreto 214/2025 está disponible aquí: Spain’s New Royal Decree 214/2025: Mandatory Carbon Footprint Reporting is Here. Este análisis demuestra cómo aquella norma ha evolucionado hasta convertirse en un plan de emergencia climática integral.

La pregunta ya no es si las empresas deben cumplir, sino con qué rapidez y estrategia lograrán adaptarse en un mundo donde el liderazgo ESG se convierte en una necesidad competitiva.

Puntos clave

De voluntario a vinculante: el decreto cerró el registro voluntario y el plan convierte el Alcance 3 en obligatorio.

Del reporte a la resiliencia: el decreto se centraba en emisiones, el plan integra adaptación y protección civil.

De cumplimiento a competitividad: España plantea el ESG como motor de inversión y liderazgo económico.

Plazos ajustados: las empresas deben reportar Alcances 1 y 2 de inmediato y prepararse en dos años para el Alcance 3.

Más exigencia, más oportunidad: un marco más estricto que el europeo, que permitirá a las empresas españolas ganar credibilidad y ventajas competitivas.

At The ESG Institute, we equip professionals and organizations to lead in this evolving landscape. Our Diploma in ESG Strategy empowers decision-makers with the knowledge and tools to integrate ESG principles into core business strategy.

Learn more and enrol: www.the-esg-institute.org/training

Leveraging a global network of over 500 experts, The ESG Institute is a leading authority in integrating Sustainability and Environment1al, Social, and Governance (ESG) principles into business strategies to drive meaningful change. With a focus on innovation and practicality, The ESG Institute provides a comprehensive suite of services, including ESG training, consulting, and certification programs. By equipping organizations with the knowledge and tools to meet evolving sustainability standards, The ESG Institute enables businesses to not only achieve compliance but also create long-term value. Its mission is to transform businesses into agents of positive change, fostering a more sustainable, equitable, and resilient global economy. For more information, visit our site.